24時間365日サポート — いつでもお客様をサポートいたします。

お問い合わせ

Patient-Centered Medical Home Market Overview, Developments & Forecast (2024-2032)

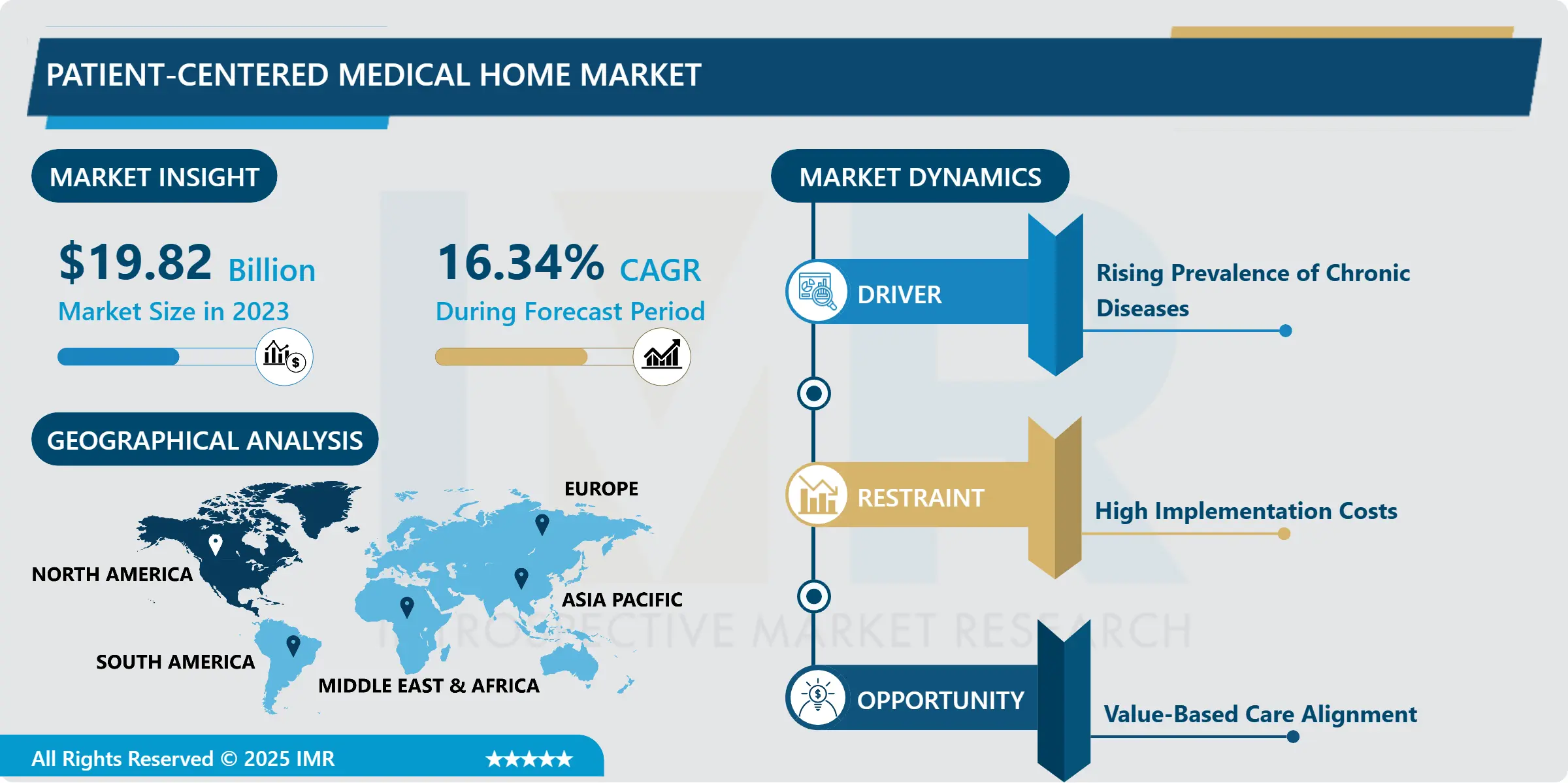

Patient-Centered Medical Home Market Size Was Valued at USD 19.82 Billion in 2023, and is Projected to Reach USD 77.39 Billion by 2032, Growing at a CAGR of 16.34% From 2024-2032. Patient Centered Medical Home (PCMH) is type of health care delivery system that is focused and planned to enhance health literacy and improve quality.

IMR

Description

Patient-Centered Medical Home Market Synopsis:

Patient-Centered Medical Home Market Size Was Valued at USD 19.82 Billion in 2023, and is Projected to Reach USD 77.39 Billion by 2032, Growing at a CAGR of 16.34% From 2024-2032.

Patient Centered Medical Home (PCMH) is type of health care delivery system that is focused and planned to enhance health literacy and improve quality. There is intended to improve the care delivery, to become patient-centered, which consists in creating deeper tie, not only to provide necessary treatments, but to also prevent the diseases and control chronic conditions. PCMHs engage different stakeholders offering health care services in ensuring that patients receive the correct type and care quality at the deserved time.

The Patient-Centered Medical Home (PCMH) model is under increasing adoption since it promises to increase the quality of healthcare services, satisfaction and reduce costs. Being centered on a concept of integrated care, PCMHs attempt at improving care coordination that is in most cases fragmented and provided by multiple professionals and settings. Primary care physicians act as gate keepers so that they be able to coordinate with other specialists, hospitals or other care givers, which in the end makes the cycle runs efficiently.

PCMHs are built on five core principles: needs include; integration, consumer orientation, organization, access and efficacy in the provision of health care to patients. Coordinated care makes sure of the different types of care—the preventive, the acute and the ongoing care are delivered. Patient-centered care means the understanding of patient’s preferences, priorities, and values while co-ordination brings about the integration of all components of health care delivery system. Accessibility is centered on increasing access to care by patients, availability of health care services for more hours in a day and use of technology based solutions. Last on the list is Quality, practiced through policies such as evidence-based practices, performance measurement and more important improvement or refining of practices.

Patient-Centered Medical Home Market Trend Analysis:

Emphasis on Digital Health Tools

The market of Patient-Centered Medical Home has several trends, one of which is constant digital health tool adoption. As the usage of new technologies becomes more popular, PCMH affiliates use EHR, telemedicine, and patient portal systems. These tools assist to make patient–clinician collaborations more effective, optimize the exchange of data and promote integration of care.

Telemedicine has made it possible for the PCMHs to reach other patients as the need to attend the health facility for checkup is minimizes. Further, patient self-service or patient portals avail our patient with our medical records, medical prescriptions, tests, etc., thus, increasing our engagement with the healthcare process. According to the development in earlier days, these digital health technologies are anticipated to make the care coordination in PCMH model much more efficient than before.

Value-Based Care Alignment

PCMH model is completely in sync with current trends of value based care which are pronounced driving forces of market growth. Professional higher payments are received depending on the health consequences experienced by the patients as opposed to how many services were delivered. PCMHs are well positioned with this model of care delivery because of their focus on prevention, stratified chronic illness and minimizing overuse of hospitals or the ER.

This alignment with value-based care motivates healthcare providers and organizations to take the PCMH model to enhance patient results at an affordable price level. For the same reasons that more and more healthcare systems are shifting toward value-based reimbursement models, there is a potential for the PCMH market to grow exponentially appealing to the stake holders of the healthcare sector.

Patient-Centered Medical Home Market Segment Analysis:

Patient-Centered Medical Home Market is Segmented on the basis of Type, Component, Mode of Delivery, End User, and Region.

By Type, Healthcare Systems/Networks segment is expected to dominate the market during the forecast period

The Patient-Centered Medical Home (PCM) model is used by different kinds of healthcare organizations and they all hold benefits. Irrespective of the differences in patient traffic and business models between Independent/Private and hospitals/Group practices, the former has key advantages in relational patient-scorp strategy and in decision autonomy making since the care is rendered in a way that caters for the patient needs that the doctor/ practice has identified. But, these large numbers of smaller organizations may have problems in adopting the PCMH model because they may not possess the finance and may be costly to manage.

On the other hand, Healthcare Systems/Networks and Government Practices have other source requirements to advance the PCMH that comprises extensive innovative technology and related care coordination systems. Another conventional actor in the PCMH market are the Community Health Centers that are mainly situated in underserved territories and focus on offering efficient comprehensive care to the resulting low-income and vulnerable population. Thus, each type of organization promotes and builds its view of the strengths and weaknesses of the PCMH model, developing market diversity.

By End User, Healthcare Providers segment expected to held the largest share

The direct stakeholders of the Patient-Centered Medical Home model include health care practitioners, patients, insurance companies and government. PCMHs are mainly launched and carried out by healthcare providers since they are the performers of most of the patient care. Particularly they gain from optimised patient satisfaction, continuity and coordination across settings for value-based care programs.

Obviously, patients benefit most from the PCMH model since their care is co-ordinated and integrated from the patient’s point of view. There are also payers and governmental institutions because they already today are shifting the attention to value-based care and payment for the services rather than for each procedure made. Engaging in the promotion of PCMH, payers and agencies of the government support changes to patient-centric medicine.

Patient-Centered Medical Home Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

North America especially the United States holds higher market growth due to compliance with technologically more developed health care structure and higher focus towards PCMH. The PCMH model is integrated in the United States by the networks of healthcare and individual practices that function according to the requirements of the model in order to better manage outcomes for their patients. CMS has been one of the key players that has encouraged PCMH through different payment ways, which are also an added market driver.

The technological development of PCMHs has been supported by the strong technology industry in North America that has ensured easy incorporation of applications to improve care coordination and patient involvement. Due to advanced adoption rates of telemedicine, EHRs, and patient portals, the PCMH model has been easy to implement in the region making it continue to dominate the market.

Active Key Players in the Patient-Centered Medical Home Market:

Aetna, Inc. (United States)

Humana, Inc. (United States)

UnitedHealth Group (United States)

Blue Cross Blue Shield Association (United States)

Anthem, Inc. (United States)

Cigna Corporation (United States)

Centene Corporation (United States)

Kaiser Permanente (United States)

Community Care of North Carolina (United States)

Blue Shield of California (United States)

National Committee for Quality Assurance (United States)

Group Health Cooperative (United States), and Other Active Players

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter’s Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Patient-Centered Medical Home Market by Type

4.1 Patient-Centered Medical Home Market Snapshot and Growth Engine

4.2 Patient-Centered Medical Home Market Overview

4.3 Independent/Private Practices

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.3.3 Key Market Trends, Growth Factors and Opportunities

4.3.4 Independent/Private Practices: Geographic Segmentation Analysis

4.4 Healthcare Systems/Networks

4.4.1 Introduction and Market Overview

4.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.4.3 Key Market Trends, Growth Factors and Opportunities

4.4.4 Healthcare Systems/Networks: Geographic Segmentation Analysis

4.5 Community Health Centers

4.5.1 Introduction and Market Overview

4.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.5.3 Key Market Trends, Growth Factors and Opportunities

4.5.4 Community Health Centers: Geographic Segmentation Analysis

4.6 Government Practices

4.6.1 Introduction and Market Overview

4.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.6.3 Key Market Trends, Growth Factors and Opportunities

4.6.4 Government Practices: Geographic Segmentation Analysis

Chapter 5: Patient-Centered Medical Home Market by Component

5.1 Patient-Centered Medical Home Market Snapshot and Growth Engine

5.2 Patient-Centered Medical Home Market Overview

5.3 Software Solutions

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.3.3 Key Market Trends, Growth Factors and Opportunities

5.3.4 Software Solutions: Geographic Segmentation Analysis

5.4 Services

5.4.1 Introduction and Market Overview

5.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.4.3 Key Market Trends, Growth Factors and Opportunities

5.4.4 Services: Geographic Segmentation Analysis

Chapter 6: Patient-Centered Medical Home Market by Mode of Delivery

6.1 Patient-Centered Medical Home Market Snapshot and Growth Engine

6.2 Patient-Centered Medical Home Market Overview

6.3 On-Premise

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.3.3 Key Market Trends, Growth Factors and Opportunities

6.3.4 On-Premise: Geographic Segmentation Analysis

6.4 Cloud-Based

6.4.1 Introduction and Market Overview

6.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.4.3 Key Market Trends, Growth Factors and Opportunities

6.4.4 Cloud-Based: Geographic Segmentation Analysis

Chapter 7: Patient-Centered Medical Home Market by End User

7.1 Patient-Centered Medical Home Market Snapshot and Growth Engine

7.2 Patient-Centered Medical Home Market Overview

7.3 Healthcare Providers

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.3.3 Key Market Trends, Growth Factors and Opportunities

7.3.4 Healthcare Providers: Geographic Segmentation Analysis

7.4 Patients

7.4.1 Introduction and Market Overview

7.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.4.3 Key Market Trends, Growth Factors and Opportunities

7.4.4 Patients: Geographic Segmentation Analysis

7.5 Payers (Insurance Companies)

7.5.1 Introduction and Market Overview

7.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.5.3 Key Market Trends, Growth Factors and Opportunities

7.5.4 Payers (Insurance Companies): Geographic Segmentation Analysis

7.6 Government Agencies

7.6.1 Introduction and Market Overview

7.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.6.3 Key Market Trends, Growth Factors and Opportunities

7.6.4 Government Agencies: Geographic Segmentation Analysis

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Patient-Centered Medical Home Market Share by Manufacturer (2023)

8.1.3 Industry BCG Matrix

8.1.4 Heat Map Analysis

8.1.5 Mergers and Acquisitions

8.2 AETNA INC. (UNITED STATES)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Key Strategic Moves and Recent Developments

8.2.10 SWOT Analysis

8.3 HUMANA INC. (UNITED STATES)

8.4 UNITEDHEALTH GROUP (UNITED STATES)

8.5 BLUE CROSS BLUE SHIELD ASSOCIATION (UNITED STATES)

8.6 ANTHEM INC. (UNITED STATES)

8.7 CIGNA CORPORATION (UNITED STATES)

8.8 CENTENE CORPORATION (UNITED STATES)

8.9 KAISER PERMANENTE (UNITED STATES)

8.10 COMMUNITY CARE OF NORTH CAROLINA (UNITED STATES)

8.11 BLUE SHIELD OF CALIFORNIA (UNITED STATES)

8.12 NATIONAL COMMITTEE FOR QUALITY ASSURANCE (UNITED STATES)

8.13 GROUP HEALTH COOPERATIVE (UNITED STATES)

8.14 OTHER ACTIVE PLAYERS

Chapter 9: Global Patient-Centered Medical Home Market By Region

9.1 Overview

9.2. North America Patient-Centered Medical Home Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecasted Market Size By Type

9.2.4.1 Independent/Private Practices

9.2.4.2 Healthcare Systems/Networks

9.2.4.3 Community Health Centers

9.2.4.4 Government Practices

9.2.5 Historic and Forecasted Market Size By Component

9.2.5.1 Software Solutions

9.2.5.2 Services

9.2.6 Historic and Forecasted Market Size By Mode of Delivery

9.2.6.1 On-Premise

9.2.6.2 Cloud-Based

9.2.7 Historic and Forecasted Market Size By End User

9.2.7.1 Healthcare Providers

9.2.7.2 Patients

9.2.7.3 Payers (Insurance Companies)

9.2.7.4 Government Agencies

9.2.8 Historic and Forecast Market Size by Country

9.2.8.1 US

9.2.8.2 Canada

9.2.8.3 Mexico

9.3. Eastern Europe Patient-Centered Medical Home Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecasted Market Size By Type

9.3.4.1 Independent/Private Practices

9.3.4.2 Healthcare Systems/Networks

9.3.4.3 Community Health Centers

9.3.4.4 Government Practices

9.3.5 Historic and Forecasted Market Size By Component

9.3.5.1 Software Solutions

9.3.5.2 Services

9.3.6 Historic and Forecasted Market Size By Mode of Delivery

9.3.6.1 On-Premise

9.3.6.2 Cloud-Based

9.3.7 Historic and Forecasted Market Size By End User

9.3.7.1 Healthcare Providers

9.3.7.2 Patients

9.3.7.3 Payers (Insurance Companies)

9.3.7.4 Government Agencies

9.3.8 Historic and Forecast Market Size by Country

9.3.8.1 Russia

9.3.8.2 Bulgaria

9.3.8.3 The Czech Republic

9.3.8.4 Hungary

9.3.8.5 Poland

9.3.8.6 Romania

9.3.8.7 Rest of Eastern Europe

9.4. Western Europe Patient-Centered Medical Home Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecasted Market Size By Type

9.4.4.1 Independent/Private Practices

9.4.4.2 Healthcare Systems/Networks

9.4.4.3 Community Health Centers

9.4.4.4 Government Practices

9.4.5 Historic and Forecasted Market Size By Component

9.4.5.1 Software Solutions

9.4.5.2 Services

9.4.6 Historic and Forecasted Market Size By Mode of Delivery

9.4.6.1 On-Premise

9.4.6.2 Cloud-Based

9.4.7 Historic and Forecasted Market Size By End User

9.4.7.1 Healthcare Providers

9.4.7.2 Patients

9.4.7.3 Payers (Insurance Companies)

9.4.7.4 Government Agencies

9.4.8 Historic and Forecast Market Size by Country

9.4.8.1 Germany

9.4.8.2 UK

9.4.8.3 France

9.4.8.4 The Netherlands

9.4.8.5 Italy

9.4.8.6 Spain

9.4.8.7 Rest of Western Europe

9.5. Asia Pacific Patient-Centered Medical Home Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecasted Market Size By Type

9.5.4.1 Independent/Private Practices

9.5.4.2 Healthcare Systems/Networks

9.5.4.3 Community Health Centers

9.5.4.4 Government Practices

9.5.5 Historic and Forecasted Market Size By Component

9.5.5.1 Software Solutions

9.5.5.2 Services

9.5.6 Historic and Forecasted Market Size By Mode of Delivery

9.5.6.1 On-Premise

9.5.6.2 Cloud-Based

9.5.7 Historic and Forecasted Market Size By End User

9.5.7.1 Healthcare Providers

9.5.7.2 Patients

9.5.7.3 Payers (Insurance Companies)

9.5.7.4 Government Agencies

9.5.8 Historic and Forecast Market Size by Country

9.5.8.1 China

9.5.8.2 India

9.5.8.3 Japan

9.5.8.4 South Korea

9.5.8.5 Malaysia

9.5.8.6 Thailand

9.5.8.7 Vietnam

9.5.8.8 The Philippines

9.5.8.9 Australia

9.5.8.10 New Zealand

9.5.8.11 Rest of APAC

9.6. Middle East & Africa Patient-Centered Medical Home Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecasted Market Size By Type

9.6.4.1 Independent/Private Practices

9.6.4.2 Healthcare Systems/Networks

9.6.4.3 Community Health Centers

9.6.4.4 Government Practices

9.6.5 Historic and Forecasted Market Size By Component

9.6.5.1 Software Solutions

9.6.5.2 Services

9.6.6 Historic and Forecasted Market Size By Mode of Delivery

9.6.6.1 On-Premise

9.6.6.2 Cloud-Based

9.6.7 Historic and Forecasted Market Size By End User

9.6.7.1 Healthcare Providers

9.6.7.2 Patients

9.6.7.3 Payers (Insurance Companies)

9.6.7.4 Government Agencies

9.6.8 Historic and Forecast Market Size by Country

9.6.8.1 Turkiye

9.6.8.2 Bahrain

9.6.8.3 Kuwait

9.6.8.4 Saudi Arabia

9.6.8.5 Qatar

9.6.8.6 UAE

9.6.8.7 Israel

9.6.8.8 South Africa

9.7. South America Patient-Centered Medical Home Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecasted Market Size By Type

9.7.4.1 Independent/Private Practices

9.7.4.2 Healthcare Systems/Networks

9.7.4.3 Community Health Centers

9.7.4.4 Government Practices

9.7.5 Historic and Forecasted Market Size By Component

9.7.5.1 Software Solutions

9.7.5.2 Services

9.7.6 Historic and Forecasted Market Size By Mode of Delivery

9.7.6.1 On-Premise

9.7.6.2 Cloud-Based

9.7.7 Historic and Forecasted Market Size By End User

9.7.7.1 Healthcare Providers

9.7.7.2 Patients

9.7.7.3 Payers (Insurance Companies)

9.7.7.4 Government Agencies

9.7.8 Historic and Forecast Market Size by Country

9.7.8.1 Brazil

9.7.8.2 Argentina

9.7.8.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

10.1 Recommendations and Concluding Analysis

10.2 Potential Market Strategies

Chapter 11 Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Q1: What would be the forecast period in the Patient-Centered Medical Home Market research report?

A1: The forecast period in the Patient-Centered Medical Home Market research report is 2024-2032.

Q2: Who are the key players in the Patient-Centered Medical Home Market?

A2: Aetna, Inc. (United States), Humana, Inc. (United States), UnitedHealth Group (United States), Blue Cross Blue Shield Association (United States), Anthem, Inc. (United States), Cigna Corporation (United States), Centene Corporation (United States), Kaiser Permanente (United States), Community Care of North Carolina (United States), Blue Shield of California (United States), National Committee for Quality Assurance (United States), Group Health Cooperative (United States), and Other Active Players.

Q3: What are the segments of the Patient-Centered Medical Home Market?

A3: The Patient-Centered Medical Home Market is segmented into Type, Component, Mode of Delivery, End User and region. By Type, the market is categorized into Independent/Private Practices, Healthcare Systems/Networks, Community Health Centers, Government Practices. By Component, the market is categorized into Software Solutions, Services. By Mode of Delivery, the market is categorized into On-Premise, Cloud-Based. By End User, the market is categorized into Healthcare Providers, Patients, Payers, Government Agencies. By region, it is analyzed across North America (U.S., Canada, Mexico), Eastern Europe (Russia, Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe), Western Europe (Germany, UK, France, Netherlands, Italy, Spain, Rest of Western Europe), Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New Zealand, Rest of APAC), Middle East & Africa (Turkiye, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa), South America (Brazil, Argentina, Rest of SA).

Q4: What is the Patient-Centered Medical Home Market?

A4: Patient Centered Medical Home (PCMH) is type of health care delivery system that is focused and planned to enhance health literacy and improve quality. There is intended to improve the care delivery, to become patient-centered, which consists in creating deeper tie, not only to provide necessary treatments, but to also prevent the diseases and control chronic conditions. PCMHs engage different stakeholders offering health care services in ensuring that patients receive the correct type and care quality at the deserved time.

Q5: How big is the Patient-Centered Medical Home Market?

A5: Patient-Centered Medical Home Market Size Was Valued at USD 19.82 Billion in 2023, and is Projected to Reach USD 77.39 Billion by 2032, Growing at a CAGR of 16.34% From 2024-2032.

How to buy a report from Megatrends.jp

On the product page, select the license you want: Single User License or Enterprise License.

Select the report language:

- English Report

- English Report + Japanese Translation

Click the Buy Now button.

You’ll be redirected to the checkout page. Enter your company and payment details.

Click Place Order to complete your purchase.

Confirmation: You’ll receive an order confirmation email. Our team will then follow up with your report delivery.

If you have questions, fill out the contact form below or email us at sales1@megatrends.jp.

Thank you for choosing Megatrends.jp!